Q4 2022 Earnings Call Transcript")

jetcityimage

After having commented on BASF’s FY outcomes, at the moment the opposite German chemical participant Evonik launched its 2022 annual replace (OTCPK:EVKIF;OTCPK:EVKIY). Right here on the Lab, in 2022, we analyzed the corporate twice offering an outperforming ranking, and we advocate that our followers check out our publications in order that they’re knowledgeable of the story thus far:

- Evonik’s initiation of protection referred to as: Earnings Defensiveness. Our purchase advice was based mostly on 1) Evonik’s internet debt place (and decrease pension contribution), 2) the Healthcare division upside with an ongoing portfolio re-reshaping, and three) a compelling valuation with a juicy dividend yield. As a reminder, the corporate’s important shareholder is a basis referred to as RAG-Stiftung. RAG has an fairness stake of 56% as of 30 January 2022 and relied upon Evonik’s dividend cost;

- Q3 outcomes remark with constructive affirmation of our Lengthy-Time period Thesis.

It was an excellent name, Evonik’s inventory value is up by greater than 23% (together with the dividend cost) and outperformed the principle index returns.

Mare Proof Lab’s earlier publication

This fall and FY 2022 outcomes

It was a difficult quarter for Evonik. Nevertheless, earlier than analyzing the This fall consequence particulars, you will need to emphasize how the corporate is transferring on with our key takeaways:

- Initially, Evonik managed to achieve its EBITDA goal (on the decrease finish, however the firm reached €2.5 billion);

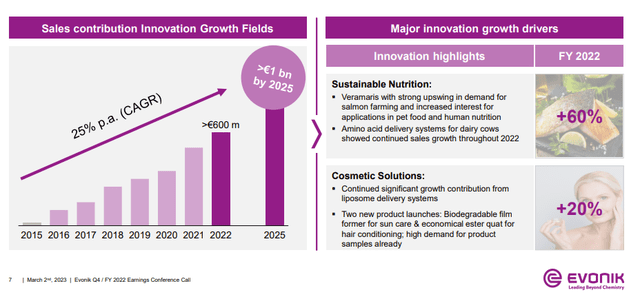

- The corporate’s portfolio reshaping is advancing. Efficiency Supplies divestments are on monitor and gross sales development within the innovation subject is up by 20% on a yearly comparability. These had been supported by diet (+20%) and beauty options (+60%) (Fig 1).

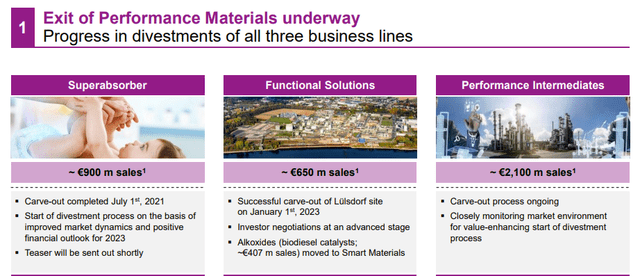

- Going deeper into the Efficiency Supplies disposal, we word that friends’ buying and selling multiples considerably decreased for decrease income development and margin stress. That is primarily because of an unfavorable macroeconomic backdrop and so this might imply a decrease exit worth. In our sum-of-the-part valuation, we now ascribe €1.7 billion in worth making use of a 2023 EV/EBITDA a number of of seven.5x (Lanxess exited its supplies enterprise for a number of near the 12x). This displays the challenges of the upcoming macroeconomic 2023 backdrop and as well as, what’s extra vital to report is the truth that if the offers will go forward, this may occasionally not create revenue for the present shareholders if adopted by expensive M&As (i.e. Air Merchandise’ Efficiency Supplies acquisition in 2016) or further funding in commodities merchandise (Fig 2). This exit is a part of the corporate’s technique to rebalance and enhance its portfolio; nonetheless, there’s a mismatch between earlier M&A monitor data and targets;

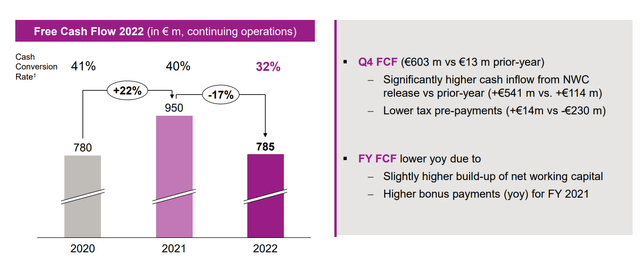

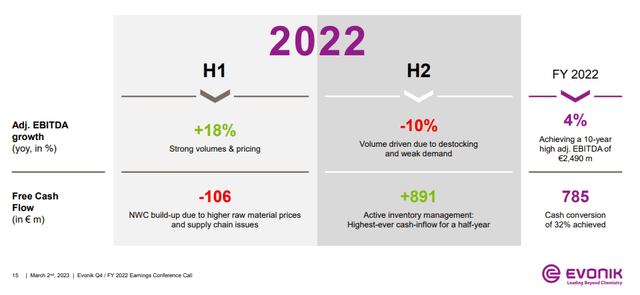

- Final time, we urged how free money movement technology was negatively impacted by increased working capital, and we had been assuming a reverse pattern. In the course of the Q3 analyst name, the CEO confirmed that “additional vital NWC enhancements are anticipated already in This fall to realize a 30% money conversion for the full-year outcomes”. Regardless of higher-than-usual inventories constructed up, the corporate managed to realize the strongest-ever quarterly FCF technology at €603 million (Fig 3).

Evonik new gross sales contribution

(Fig 1)

Evonik PM Exit

(Fig 2)

Evonik FCF evolution

(Fig 3)

Wanting on the monetary efficiency, Evonik delivered a combined quarter. Following a yr of provide chain points, This fall chemical compounds quantity continued to say no primarily because of shoppers destocking from earlier excessive ranges. Having checked BASF, European chemical manufacturing was 18% decrease in comparison with final yr’s finish quarter, Evonik was in a position to be extra resilient, and regardless of a unfavourable consequence and a GEO presence extra skewed in the direction of the EU, closed This fall with a minus 11%.

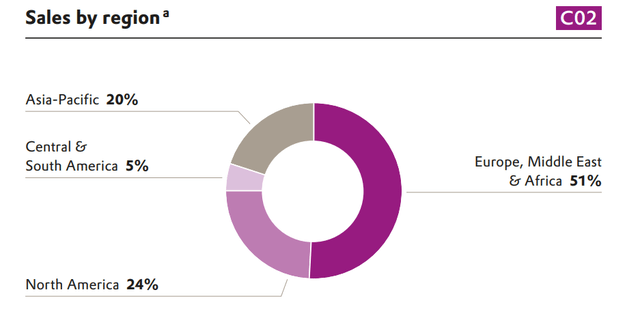

Evonik GEO gross sales

The corporate’s monetary debt stood at €3.25 billion and was decrease from the Q3 degree due to divestment proceeds such because the betaine operations US and TAA derivatives. As well as, pension provisions additional declined to €1.35 billion due to an additional enhance within the low cost charge (now at 4.1%). To sum up, Evonik’s leverage on the web debt/EBITDA reached 1.8x from 2.7x within the 2021 year-end.

Evonik Financials in a Snap

Conclusion and Valuation

Concerning the 2023 outlook, Evonik is forecasting top-line gross sales between €17 and 19 billion with an adjusted EBITDA between €2.1 and a pair of.4 billion. This steerage is predicated on a weak H1 and a stronger H2. As already talked about in BASF, the corporate is implying a major tailwind in China and an bettering demand in Europe within the second a part of the yr; nonetheless, neither of those is clear at this level. What’s vital to report is the truth that Evonik is concentrating on natural development above 3.5% and an EBITDA margin enhance. If we’re trying on the previous monetary efficiency, the agency income development was simply 1.5% within the 2015-2020 interval and the EBITDA margin decreased to fifteen.9% in 2021 from 18.2% in 2015. Because of this, earnings development has been restricted and the corporate has needed to purchase new sources of working money movement, and as a consequence, returns have been beneath stress. The dividend was confirmed (and we’re not stunned) and persevering with to worth Evonik with a 6x EV/EBITDA on 2023 accounts (contemplating additionally a €1.7 billion in proceeds from PM exit), we determined to keep up our goal value of €23 per share ($12.25 in ADR). On an EV/EBITDA foundation, Evonik is buying and selling at 15% in comparison with its closest friends. Our dangers embrace increased capability addition from opponents in addition to the chance of potential M&A worth destruction.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please pay attention to the dangers related to these shares.