Q4 2022 Earnings Call Transcript")

courtneyk

Co-produced with Treading Softly

How will you have a “wealthy retirement?” To be wealthy means to have an ample provide of money, capital, or a excessive internet price. One of the simplest ways to generate such an overage is to have a excessive money movement into your brokerage accounts.

Being rich means having a big sufficient asset base that the earnings it produces exceeds your bills. This lets you take the surplus earnings and reinvest it into extra income-producing property. As your wealth grows, so does your earnings. Nothing fairly makes cash, as cash does.

I’ve written quite a few occasions about how being rich will routinely default you into being wealthy as a byproduct, however being wealthy doesn’t imply you might be rich. Multiple individual with a $1 million+ earnings managed to blow all of it.

For a wealthy retirement, you both wanted to have stockpiled these extra {dollars} throughout all of your working years, or it’s essential to discover a means to generate a excessive degree of earnings now – hopefully with out working!

My private funding philosophy – The Revenue Technique – makes use of fast earnings investing as a way to generate a excessive degree of earnings at this time to fulfill your bills head-on. Most significantly, you’ll be able to present a excessive sufficient earnings that you’ve got an extra to reinvest and develop your asset base additional.

Right this moment, I need to take a look at two nice alternatives to take pleasure in a wealthy retirement via the earnings they supply.

Let’s dive in.

Choose #1: GHI – Yield 8.8%

Greystone Housing Influence Buyers, LP (GHI) had an unbelievable 2022, ending the yr with CAD (Money Accessible for Distribution) of $2.37/unit. This led GHI to pay out supplemental distributions for a complete distribution of $2.109/unit for the yr. That could be a realized yield that’s nicely into the double-digits on the costs GHI traded at all year long.

Do not get used to it. Going ahead, we should always anticipate payouts to be a lot nearer to the “common” distribution, which is about at $0.37/quarter. $1.48/yr is a extra correct reflection of the distribution that buyers can anticipate to be recurring.

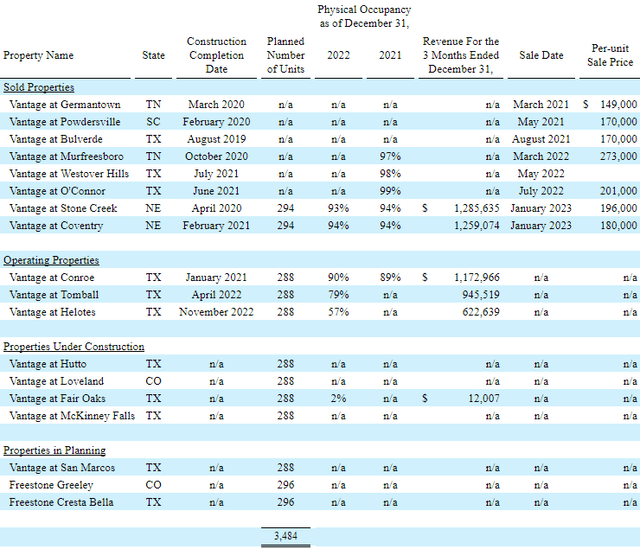

We will thank GHI’s “Vantage” three way partnership for the surplus distributions in 2022. They realized $39.7 million in capital beneficial properties promoting properties in 2022, and GHI handed alongside a considerable portion of these beneficial properties to buyers.

The Vantage JV follows a technique of growing flats, renting the models, and promoting them when occupancy stabilizes. It usually takes about three years for this course of to occur. In consequence, the proceeds from these gross sales are lumpy, however are additionally extraordinarily profitable. Buyers are completely happy to pay a premium for a property that’s already leased up and all of the exhausting work has been finished. GHI performs the position of offering capital, with a most popular funding that recovers a set quantity, after which the companions cut up the beneficial properties after the popular funding is paid off.

Final yr, circumstances have been exceptionally favorable to be promoting flats. Hire was rising and rates of interest have been nonetheless low within the first half of the yr when most of those gross sales occurred. Right this moment, rents are slowing down and rates of interest are excessive. Nevertheless, regardless of that, the JV did handle to understand gross sales of two properties, paying GHI a $244k most popular return, plus $15.2 million in capital beneficial properties (about $0.67/unit).

This technique has been very profitable for GHI, and it’s increasing it. There are three extra properties the place building is accomplished and leasing is underway (Conroe was introduced listed on the market on March sixth), 4 extra which are below building, and three which are within the planning levels. Supply

GHI 2022 10-Okay

This may be sure that GHI has a gentle pipeline of properties that might be bought. The issue is, that you could’t management when a purchaser desires to purchase. The final two gross sales bought at $196,000 and $180,000/unit. That is decrease than the costs that the JV was capable of obtain final yr however nonetheless greater than seen in 2021.

With rates of interest greater and lots of uncertainty concerning the financial system, any extra gross sales closed this yr must be thought of a cherry on high. The excellent news is that the gross sales already closed present lots of cushion for the distribution payout, and it’d even present sufficient for a small complement/particular at year-end.

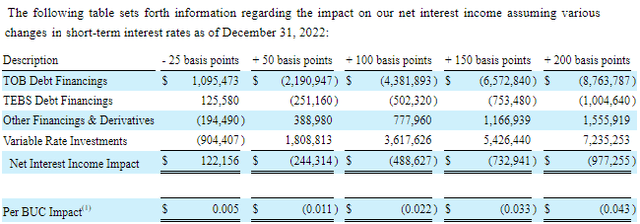

GHI’s different core enterprise is investing in “mortgage income bonds”, these are bonds issued to builders who’re constructing low-income housing. The decline in bond costs has impacted the MRB market, similar to it has each different kind of debt. This has been a headwind to e book worth, and rising rates of interest are a slight headwind to earnings. GHI has hedged itself very nicely, however one other 100 bps in charge hikes would scale back earnings by roughly $0.022/unit for the yr.

GHI 2022 10-Okay

The excellent news is that if rates of interest began coming down, GHI would profit from this portion of the enterprise. Greater yields scale back the worth of held loans, nevertheless it additionally makes it cheaper to purchase new loans. GHI’s most up-to-date MRBs have coupons of round 6.5%.

GHI is a good selection for an funding that might profit from declining rates of interest, however has proven nice resilience in holding as much as rising charges. We will thank the Vantage JV technique for that. The mixture of two methods which are fully totally different, creates an organization that’s able to producing a fantastic return in any setting. We won’t depend on $2+ in distributions for 2023, however we might be very assured that the $1.48 in common distributions is sustainable.

Choose #2: GLP-B Most well-liked – Yield 9.3%

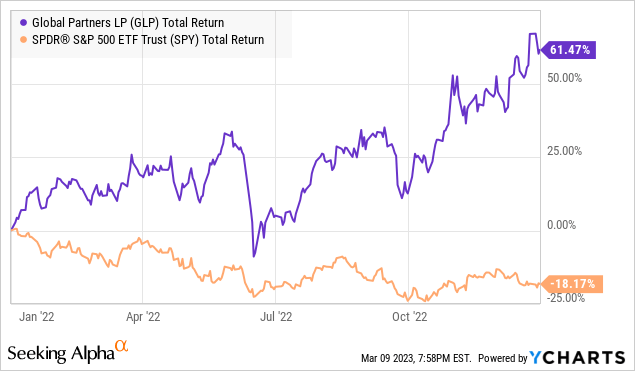

International Companions LP (GLP) is a big gas distribution grasp restricted partnership that has strongly rewarded its buyers via all of 2022.

GLP strongly trounced the general market as a consequence of increasing gas margins. GLP, via its wholesale and retail gas distribution and comfort retailer community, loved robust returns as gas demand picked up, and gasoline costs climbed swiftly via 2022.

GLP advantages from shopping for gasoline at wholesale costs, and when costs rise as they transfer it to their gasoline stations, they profit from the upper value. Moreover, the comfort retailer sector is essentially fractured with many small mom-and-pop operations, so when costs rise after which fall once more, these small areas are unable to afford to drop costs. This enables GLP to match their costs whereas benefiting from shifting extra quantity than their opponents.

This all added as much as a banner yr for GLP and different gas distributors. GLP lined their widespread distributions by 2.6x after factoring in the popular dividends over the course of 2022. This contains their giant particular distribution.

Nevertheless, at the moment, GLP’s widespread shares are more likely to see a retracement of their climb greater. GLP’s widespread yield is at the moment simply over 7%. So why can we anticipate GLP’s widespread shares to fall in worth? The important thing metric to observe is gas margins – the costs GLP gleans from the value they pay for gas and the value they cost.

GLP’s administration is forecasting, and forewarning of a drop on this margin in 2023 as gas demand and gasoline costs normalize:

So I feel we’re — our expectations and who is aware of what is going on to occur ahead. Our expectations, as we sit right here at this time, our margins ought to — and we’ve seen this, margins ought to return again in direction of one thing extra regular because the curve has flattened, as volatility has quieted down and as the price of carrying stock has decreased.

We have seen a corresponding downshift in margins in direction of extra of a historic norm, though nonetheless at elevated ranges. And with out figuring out what is going on to occur subsequent, I feel as you look out the curve, it is cheap to imagine that these are the market circumstances that we will be coping with for the steadiness of ’23. Now clearly, if there’s some kind of occasion or demand is stronger than anticipated, which I really feel just like the bias is that it’ll underperform, not overperform. However any occasion, I might say inventories are nonetheless on the tighter aspect. So any occasion might ship that in a special route. However as we — based mostly on our visibility proper now, we’re beginning to see issues pattern extra in direction of historic norms than what we noticed in 2022. – GLP Incomes Name Transcript

This drop in margin, tied together with greater bills as a consequence of inflation, will put a squeeze on GLP’s general distribution protection. We don’t anticipate GLP must lower its widespread distribution – they elected to do a big particular vs. an enormous common hike, which was sensible in our analysis. Nevertheless, because the market sees GLP’s earnings underperforming year-over-year, we anticipate promoting stress to speed up.

So if we’re uninterested within the widespread shares because of the poor year-over-year comparisons to return, the place do we discover enticing yields from GLP?

Their most popular securities supply enticing risk-adjusted returns. International Companions, 9.50% Collection B Mounted Charge Cumulative Redeemable Perpetual Most well-liked Models (GLP.PB) at the moment commerce over PAR however supply a excessive fastened yield at 9.3%. We discover these extra enticing than GLP’s different most popular providing at the moment, which trades at a wider premium and has a floating interest-rate element. GLP can name International Companions, 9.75% Collection A Mounted-to-Float Cumulative Redeemable Perpetual Most well-liked Models (GLP.PA) in August and is already contemplating tapping the bond market to repay a latest acquisition. Tacking on the wanted funds to name GLP-A could be simply finished as nicely.

GLP-B can’t be known as till 2026, offering a wholesome yield-to-call of 9%. GLP’s skill to pay their most popular dividends shouldn’t be in query with their robust widespread dividend protection. So we discover GLP-B to be exceptionally enticing at the moment.

The world wants gasoline and diesel to get from level A to level B. Do you’ve got an EV? GLP is routinely including EV charging stations to their areas as nicely. The world is stopping to go to their areas, and GLP supplies me with a wholesome earnings.

Conclusion

GHI and GLP-B supply excessive ranges of earnings which you’ll depend on and luxuriate in. This regular movement of high-yield earnings will proceed in good occasions and unhealthy, which all of us need once we know life throws curveballs repeatedly.

For a few of us, a “wealthy retirement” is not money-centric in any respect, however cash is usually the oil that lubricates the gears in life. It is exhausting to have enjoyable or take pleasure in life when monetary woes are piling up or looming throughout us. I need you to have the most effective retirement doable, and these two picks will help you obtain that!

That is the great thing about earnings investing.