Q4 2022 Earnings Call Transcript")

DNY59

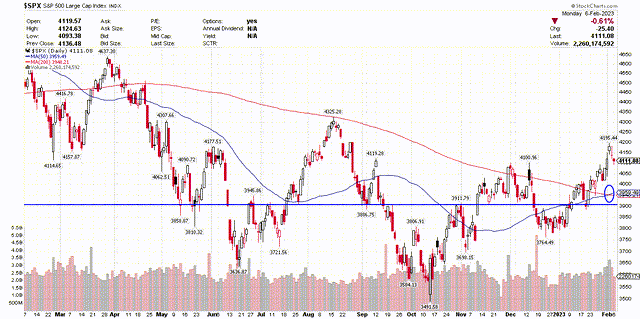

A deeply oversold market wherein sentiment was abysmal, rates of interest have been peaking, and the speed of inflation was beginning to recede led to an incredible rally over the previous 5 months. That rally gave the impression to be dropping steam in early February, coincident with a Golden Cross for the S&P 500, which happens when the 50-day transferring common crosses above the 200-day transferring common, as will be seen within the chart beneath. At the moment, I urged traders put together for a pullback to 3,900 in what could be a pause to refresh the uptrend. It was prone to be instigated by hawkish rhetoric from Fed officers in response to strengthening financial information that started with the January jobs report. That’s precisely what has occurred.

Edward Jones

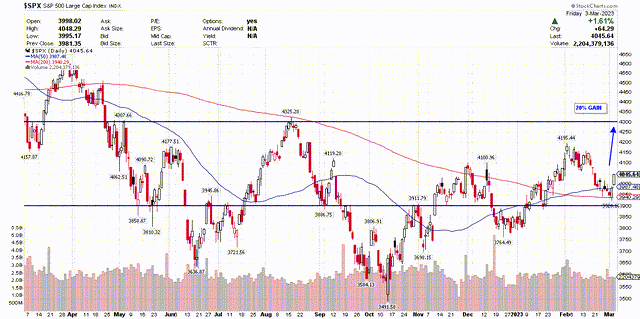

I didn’t use valuations to reach at my goal of three,900 for the index, however a technical vary of three,950 to three,983 with the excessive chance of an overshoot. The Golden Cross occurred at 3,950, whereas three completely different breadth indicators triggered purchase indicators at 3,983 a number of weeks earlier. Subsequently, it made sense that this vary could be examined with any overshoot beneath that vary aggressively purchased. The low final week was 3,928 on an intraday foundation and aggressively purchased it was, as we closed at 4,045 on Friday.

Stockcharts

Now I’m getting ready for a rally to 4,300, which might full a bull market run of 20% off the October closing low of three,577, however I feel it will likely be conditioned on a reversal of the components that led to the selloff. We must always see a lot softer financial information for February, which I anticipate will begin with this Friday’s jobs report and be adopted with extra modest retail gross sales and shopper spending figures. Not solely is the speed of financial development slowing from the financial coverage tightening to this point, however January’s information was boosted considerably by seasonal changes that made it look a lot stronger. The changes is not going to be a consider February.

Stockcharts

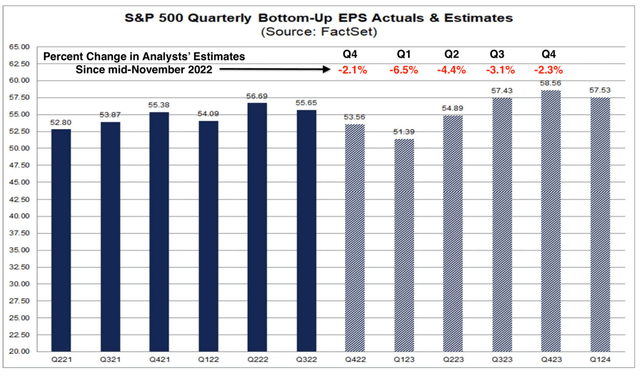

Weaker information ought to welcome a much less hawkish tone from Fed officers, a softer greenback, and a decline in rates of interest throughout the yield curve. All of those developments would assist to assist inventory valuations, as traders look previous the trough in company earnings that analysts see within the present quarter.

DataTrek

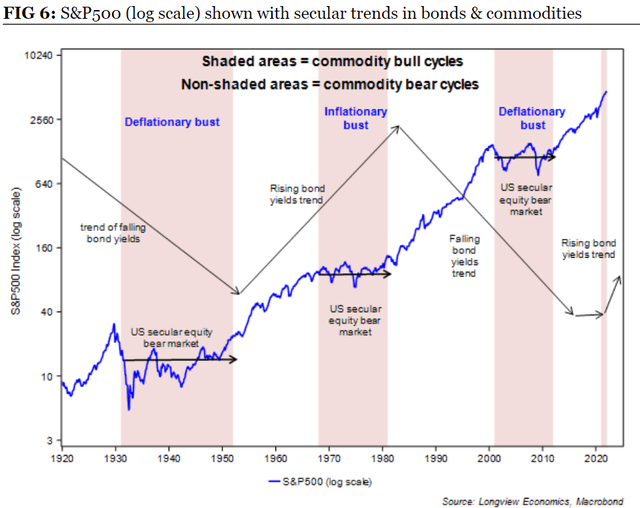

I’m not ignoring financial or market fundamentals when navigating the market’s actions over a 6-12 month time-frame, as I absolutely acknowledge the headwinds right this moment’s lofty valuations current. As an alternative, I place extra emphasis on them when contemplating my long run outlook. I shared the chart beneath with readers one 12 months in the past when asserting that we have been doubtless headed for an additional misplaced decade, because it pertains to broad inventory market returns. Monetary markets are adjusting to the tip of free cash, in any other case generally known as near-zero-interest-rates, in addition to the medicinal drip of quantitative easing, which went on intermittently for greater than a decade. That adjustment course of might take years, and it’s prone to maintain the S&P 500 trapped in a really large buying and selling vary that leads to a secular bear market much like what we noticed from 2000 to 2010.

Bloomberg

But that doesn’t imply traders ought to eradicate inventory publicity and pile into short-term Treasuries yielding 5%. There have been super bull runs throughout the 2000s that lasted for much longer than 12 months. The distinction now’s that the bond market presents enticing alternate options to shares for extra threat averse traders. Passive investing is prone to lose its luster, whereas inventory choosing falls again into favor, which favors tactical funding methods. This implies various publicity to shares, bonds, commodities, and money over time as we transfer by means of the varied phases of the enterprise cycle.