Q4 2022 Earnings Call Transcript")

Systematic Revenue CEF Instrument

This text was first launched to Systematic Revenue subscribers and free trials on Mar. 4.

Welcome to a different installment of our CEF Market Weekly Assessment the place we focus on closed-end fund (“CEF”) market exercise from each the bottom-up – highlighting particular person fund information and occasions – in addition to the top-down – offering an outline of the broader market. We additionally attempt to present some historic context in addition to the related themes that look to be driving markets or that buyers must be conscious of.

This replace covers the interval by the primary week of March. Make sure to take a look at our different weekly updates protecting the enterprise growth firm (“BDC”) in addition to the preferreds/child bond markets for views throughout the broader earnings area.

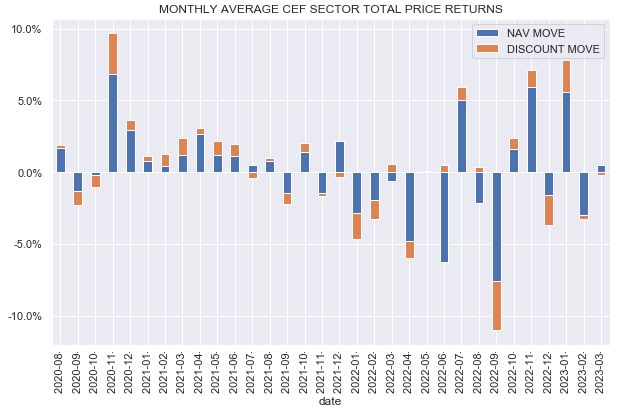

Market Motion

CEFs completed largely within the inexperienced this week, turning round a stretch of a number of down weeks in a row. Greater-quality / longer-duration sectors like Munis and Funding-grade bond funds underperformed.

February shaved off round half of the January rally as resilient macro and inflation indicators triggered the market to reassess the extent of the terminal Fed coverage fee.

Systematic Revenue

Reductions widened just lately however proceed to commerce round their longer-term fair-value vary.

Systematic Revenue

The latest weak point throughout CEFs is basically as a result of back-up in Treasury yields as credit score spreads have been very effectively behaved. Excessive-yield credit score spreads are almost 2% off their 2022 peak ranges and replicate the general resilience of the broader economic system. This retains us centered on higher-quality property throughout the yield curve in the mean time so far as new capital allocations.

Systematic Revenue

Market Themes

Given the stress on asset costs because the begin of 2022 and its affect on investor portfolios, an affordable query is whether or not we are able to anticipate CEF costs to retrace their earlier ranges.

The chart under exhibits normalized costs of the favored PIMCO taxable CEFs from 2020 which highlights that we’re fairly a approach off ranges initially of 2022. These funds are removed from the one ones buying and selling effectively under their early-2022 ranges.

Systematic Revenue

To get a greater instinct about this necessary query, we have to take into account all the important thing drivers of CEF costs. These are reductions, leverage, charges and credit score spreads (for length property, credit score spreads provided that we’re speaking about floating fee credit score property and fairness costs for fairness CEFs) which we are able to seek advice from as unrealized good points or losses, the yield vs. distribution differential, and realized good points (or losses).

Beginning with rates of interest, we’re effectively off the 1.3% start line for 5Y Treasuries and it appears unlikely we’ll revisit that degree any time quickly, barring a black swan sort of occasion.

FRED

If we use high-yield company bonds as our credit score unfold proxy then spreads look fairly a bit higher, having retraced near 2/3 of the rise from 2022. A really delicate touchdown will seemingly push spreads tighter from right here nonetheless even a gentle recession is more likely to push them wider.

FRED

So far as reductions, they’re wider from their 2022-start ranges with fixed-income CEF reductions having widened greater than their fairness counterparts. Reductions are largely pushed by distribution adjustments, returns and total danger sentiment. It is very possible that in a powerful market surroundings we see a full or a virtually full low cost retracement to earlier ranges.

Systematic Revenue

Turning to leverage, many leveraged CEFs have deleveraged this yr below stress from falling costs since falling costs mechanically elevate the extent of fund leverage. A deleveraging itself doesn’t should drive financial losses nevertheless it usually does as a result of funds are slower so as to add borrowings when asset costs begin to retrace which locks in financial losses. All else equal, funds which have deleveraged are unlikely to see their NAVs retrace to beginning ranges although this financial hole is more likely to be modest.

The yield vs. distribution differential refers to below or over-distribution by a given CEF. Right here we concentrate on portfolio yield fairly than web earnings which is a crucial level. Funds that overdistribute relative to their portfolio yield will are likely to see their NAV fall, all else equal and vice-versa. Relative to their 2022-start portfolio yields, most CEFs have been overdistributing which is why this dynamic will weigh on NAVs, all else equal, notably over the long run.

Lastly, realized good points or losses can occur on account of issues like defaults in credit score portfolios or buying and selling losses i.e. shopping for excessive and promoting low. Credit score and buying and selling losses are troublesome to keep away from even by robust managers, nonetheless, this may be doubtlessly offset by good points i.e. alpha.

General, our view is that the majority credit score CEFs are most unlikely to see a retracement again to their 2022-start NAV and worth ranges. The important thing components are that rates of interest are unlikely to completely retrace and deleveraging has locked in some financial losses for funds. That stated, costs have tended to maneuver decrease over time for credit score CEFs anyway – a characteristic which worries some buyers however is simply the price of admission to credit score property.

Unleveraged fairness CEFs have one of the best probability to retrace their earlier worth ranges nonetheless these funds are troublesome to name correct earnings property (until buyers are additionally prepared to name SPX trackers earnings securities).

Market Commentary

Nuveen launched a February CEF distribution replace. There was a drop within the JHAA distribution which isn’t sudden given it’s a time period CEF. There have been additionally cuts within the month-to-month managed distribution CEFs (e.g. NDMO) and quarterly managed distribution funds (JCE, QQQX, JRS, NMAI).

Nuveen has a jumble of various managed distribution insurance policies aside from most of its CEFs which don’t have managed distributions. A “degree distribution” applies largely to company credit score and mortgage CEFs which is odd given many of those funds are both totally or considerably in floating-rate property.

There are additionally the “month-to-month” and “quarterly managed distribution” funds with quarterly funds being equity-oriented. It’s under no circumstances clear why a reasonably generic Muni fund like NDMO can be in a managed distribution group whereas all different Nuveen Muni CEFs are within the unmanaged bucket.

Previous to the minimize, NDMO had an unusually excessive distribution fee for a Muni CEF although Part 19 confirmed half of the distribution was ROC. Maybe the concept behind placing NDMO into the managed distribution bucket was to recommend that the “Dynamic Alternatives” a part of the title would have the ability to generate extra capital good points to help the elevated distribution. To this point this hasn’t labored out. The fund stays costly regardless of its underperformance in whole NAV phrases.

Systematic Revenue CEF Instrument